rinehimerbaker’s Year-in-Review

Take a glimpse at rinehimerbaker’s year-in-review as we get ready to take on 2020.

rinehimerbaker’s Year in Review – Made with Moovly

Take a glimpse at rinehimerbaker’s year-in-review as we get ready to take on 2020.

rinehimerbaker’s Year in Review – Made with Moovly

Some big news from the team at rinehimerbaker. Earlier this month, we were named the Sage Intacct Partner of the Quarter for our strong sales performance and high levels of ongoing customer satisfaction. Learn what this means for our prospects and customers below. Read more

The benefits of cloud-based software are usually cited as lower costs, process and workflow optimization, and scalability. But the attraction and retention of key finance and accounting department personnel is another benefit of implementing the best-in-class technology—one that’s not included in the “top 5 benefits” lists, but should be. The reality is that today’s top financial talent—and tomorrow’s leaders—operate in a digital world, where 24/7 access, insight, and productivity reign. Read more

Remember the “no-internet policy?” It wasn’t so long ago that companies were keeping their employees from exploring the world wide web on company machines. But as all-things-internet have become ubiquitous, including mobile devices and, yes, cloud computing in the workplace, hopping online to get things done—to perform essential professional tasks, let alone browse favorite website—is commonplace. No wonder Gartner reports that by 2020, a corporate “no-cloud” policy will become as rare as a “no-internet” policy is today. Read more

Being successful as a nonprofit means that everything needs to fall into place when and where it needs to fall into place. Knowing this, there are many different considerations and moving parts that you can control in order to gain additional visibility, save time, and improve outcomes.

While we discussed some of these factors, including the shift to outcome metrics and things to understand before selecting or changing from a calendar year to a fiscal one, today, we would like to turn our attention to another important consideration: How to choose a basis of accounting.

A recent AICPA article explored the basics on selecting a basis, and how to decide on whether a cash basis, accrual basis, modified cash basis, or tax basis is the proper way to look at the numbers, comparing these options and offering tips on how to select the one that makes the most sense to your nonprofit.

Whether cash, accrual, modified, or tax year, each basis of accounting listed below poses opportunities and challenges in measurement, disclosure, and reporting.

If a nonprofit organization uses the cash method of preparing its accounting records and statements, it recognizes income and expenses when they occur. In other words, the nonprofit would record income when it received the funds and not when it is actually earned. It would also record expenses at the time it paid the bill rather than when it incurred the expense.

This is a common approach for smaller nonprofits, as it mirrors a personal “checkbook accounting,” entering debits or credits as they are completed. For example, under a cash basis, if you receive a $10,000 pledge today, you do not record the $10,000 until the money is in the bank.

Pros and cons of the cash basis are as follows:

Using the accrual method of accounting, a nonprofit recognizes income when they earn it, rather than when they receive it. It would also recognize expenses when they were incurred instead of when the organization paid the bill. For example, using the accrual method a nonprofit would recognize a pledge as income. That would hold true even if it had not yet received all the money, or even any amount of the donation pledged.

Under the accrual method, nonprofits would record revenue and expenses when the transaction takes place, regardless of whether the cash has changed hands. For example, a $10,000 pledge would be recorded immediately and would create a receivables account for outstanding cash.

Funds accounting is a form of accrual accounting that is specific to nonprofits. As a nonprofit grows, its funding sources can become more diversified. It may receive multiple grants, a government contract, personal donations of cash and goods and donations of time. With the funds basis of accrual accounting, each income stream is given its own accounting code. For example, your Department of Education grant would have its own code. Beyond that, you would be able to assign codes within a category so that you could break up DOE funds between general revenue, service revenue and administrative.

Modified cash basis statements combine elements of cash basis and accrual accounting. Certain transactions are reported on an accrual basis and others on a cash basis (for example, liabilities may be presented, but fixed assets may not).

The modified cash basis establishes a position part way between the cash and accrual methods. The modified basis has the following features:

While rare in the nonprofit world, there may be some cases for a tax basis for accounting. The tax method of accounting would ensure the financial statements match the organization’s Form 990.

AICPA author Marc Kotsonas, CPA, Officer- Mahoney Ulbrich Christiansen Russ shared the following six factors in choosing a basis of accounting.

At rinehimerbaker, we are committed to helping you succeed. This is why we have written a series of helpful articles on running the finances at a nonprofit organization. We invite you to learn more by reading our articles on Outcome measures, improving reporting, and increasing efficiency. Learn even more by reading these two nonprofit success stories from our friends at Sage Intacct, and contact us for more details.

Contrary to popular belief, the nine most terrifying words in the English language are not always “I’m from the government and I’m here to help.” For small business finance and accounting professionals, there is another phrase that strikes even more fear, anger and disdain: “QuickBooks has stopped working and must be shut down.”

So how do you go about trying to tackle the problem? You run a clean reinstall. You download the diagnostic tool. You run a second clean reinstall. You attempt to run it without antivirus. You rename the .tlg file. You update it, you repair it, you download every tool in the book, and you still see those nine terrifying words: “QuickBooks has stopped working and must be shut down.”

It’s infuriating. It’s painful. It happens over and over and over. Those nine terrifying words are etched in your memory. Yet it’s all too common. You search the knowledge base for answers, and you see that you’re not alone. A quick Google search for the exact phrase “QuickBooks has Stopped Working” yields 959 results on the Intuit Community alone, and over 16,000 results across the web.

So when is QuickBooks most likely to crash? As a company that has helped many companies outgrowing QuickBooks to make the move, we have heard many complaints about the platform.

However, it’s not only the crashes that present a problem. QuickBooks might run slowly in multi-user mode. It might run slowly if your audit trail gets too long. It might run slowly when your data file gets too big.

There are many reasons for this. Some of the most commonly referenced ones on the Intuit Community:

For a software that’s been around as long as QuickBooks has, there’s certainly a lot that can go wrong.

QuickBooks users around the world face the same struggles—especially as it pertains to the software crashing. Unfortunately, there are two reasons that you will continue to face problems.

QuickBooks was built as a desktop application, which is why most of the reasons above revolve around computer and file-based issues. This is something that isn’t going to change. Anything from a change in operating system to the use of an anti-virus software can derail the entire QuickBooks desktop experience, causing crashes and other poor experiences.

It was initially thought that QuickBooks would address this when it introduced QuickBooks Online, but customers quickly found that it didn’t hold up to customer expectations. QuickBooks wasn’t built to be an online application, so when Intuit tried to rebuild QuickBooks for the web, it ended up putting up a web application that is lacking, according to G2Crowd reviews.

QuickBooks’ other fatal flaw—at least as it pertains to growing businesses, is that you’re asking it to do too much. Just as QuickBooks was designed to be a desktop software (i.e. run on a personal computer), QuickBooks was designed to make life easier for the small business owner. Again, we’ve said it on our blog before—QuickBooks is great for small businesses. It’s the larger businesses that push the software to (and past) its limitations.

While not always why the software crashes, a large file size is one of the main reasons that the software runs slowly. Also, as the file size grows, so does the risk and impact of the file being corrupted.

Barring an unfortunate turn of events, the latter of these two isn’t going to change—once you’ve outgrown QuickBooks, there’s no looking back.

When your business was just starting up, adopting QuickBooks was almost a rite of passage. It was a welcome sign of your company’s growth and the accounting system met your needs for a time. But your business has kept growing, and now you’re seeing the limitations of the system you once depended on. QuickBooks simply doesn’t offer all the capabilities you need today—or tomorrow. The time has come, once again, for a change.

We invite you to learn more about additional warning signs, pain points, and opportunities for improvement from downloading our guide for companies outgrowing QuickBooks, which you can preview below.

If you’re outgrowing QuickBooks or simply looking to simplify and automate your processes by moving accounting to the cloud, the process for building a long list and then narrowing it down to a short list can be a challenge. As part of the narrowing-down process, you will spend a lot of time demoing the software and discussing it with the sales team for each vendor.

As you narrow down your options, it’s important to understand what you’re looking for and how the solution will fit into the equation. This is why we have developed a non-exhaustive list of important questions to ask—and what you should expect in terms of an answer.

The uptime discussion is one of the main things that can separate vendors, and should be one of the first things you look for. Uptime is generally discussed in terms of “nines,” as in “how many nines can you promise,” and shouldn’t be taken lightly, as each nine promised is a testament to the company’s commitment to the customer:

While five or more nines is often reserved (and priced) for mission critical applications like telecommunications, utilities, and more, your cloud provider should be able to promise and deliver more than two nines. Often, the sweet spot for SaaS applications is right around three nines, meaning you will see no more than ten minutes of unplanned downtime per month.

However, the real way to judge a vendor is not by promises made, but promises kept. For instance, a leading vendor in the cloud space promises 99.8% uptime, but delivers a 12-month rolling average of 99.987%—nearing the five nines “promised land.”

While the answer is probably yes (the cloud accounting and ERP market is relatively mature), the real question you should be asking is “have you had success with our industry?” It’s common for a vendor to have product or service pages for many different industries, but few case studies pertaining to the industries. It’s important to look at these case studies and success stories for companies like yours in size, needs, and industry.

Another of the natural advantages of a cloud-based accounting software, there are still differences in start-up pricing and implementation. This is an example in which time is quite literally money, as you will be charged for each hour of migration, training, and other necessary services.

The biggest differentiator in this equation is the scope of the implementation—how deep will the software reach into your organization? Suites will naturally take longer to implement, but it will be a one-time project. Single-focus best-of-breed applications can be done quickly and easily, but you may have to complete multiple, less disruptive projects. We discuss the Implementation process in our blog series, Eight Things to Look for in Accounting Software, Part 2.

Pricing is one of the key advantages of SaaS-based applications, generally allowing a move away from licenses, which in turn helps to offer more transparency and ease decision-making. With this in mind, as you compare vendors, one of the most common structures you will see is the per-user, per-module pricing.

In this, it’s important to know what you’re getting, how much it will cost, and how much it will cost for additional users—some users will need additional access, functionality, and modules. Know what you’re getting, how much you’ll be paying, and how much it will cost to add users, modules, or more as your business expands.

At some point, you’ll be using a software, and think, “wow, wouldn’t it be nice if I can do [this]” or “how much easier would my job be if the software could do [this]?” One of the advantages of the cloud is that updates are much more flexible and frequent. Rather than having to wait a year for new patches, cloud accounting applications offer much more frequent updates—up to four times a year.

Knowing this, it’s important to understand the process for requesting new features. Is it easy to ask? Will you be given the same opportunity to request as a large business? How does the vendor narrow down what will be added in the release?

As we said, cloud software updates more frequently and easily than an on-premises offering (updates are hands-off; often you walk in to an update the next day or on a Monday). However, the more moving parts that a software has, the less frequent or focused an update will be. This is a main difference between suites and best of breed offerings—suites add a lot of complexity to the equation, so R&D money is spread across multiple products.

When you look to change accounting software, it’s just as important to plan as it is to find the right software. If you know what you want, you will be able to narrow down vendors with minimal stress. Stay tuned for an upcoming blog in which we discuss some of the internal discussions you will need to have before you even start looking at new cloud solutions, coming early next month. If you’re ready to learn more about the power of Sage Intacct for your growing business, contact us today.

With just over a year to go for private companies to have their ASC 606 plans in place, many organizations are yet to have done much to get the ball rolling. This is why we began this series, to introduce you to the various steps involved in recognizing revenue under the new standard.

As part of an ongoing series, we are breaking down the 156-page standard and providing key takeaways, including who ASC 606 affects, a brief overview on the five steps, and a look at how ASC 606 will affect different industries, but today we would like to introduce a deeper look at each step:

Biggest Impacts: Software, Telecommunications

With considerations including standalone selling price, allocating discounts and variable consideration, and changes in the transaction price, there are certain pitfalls in allocating price to each obligation.

After Step 3, determining the transaction price as a whole, you will need to determine the standalone selling price of each good and/or service promised in step 4. As is often the case, the way to do this is to determine the price based on standalone sales of the good or service to similarly situated customers.

However, this is not often observable. When this is the case, a seller is to determine standalone prices in one of three ways:

Oddly, for US-based businesses, the new standard will provide more flexibility for organizations than the previous standard, a rare occurrence within ASC 606 according to the KPMG Revenue Issues in Depth Article. Under the current standard, standalone selling prices are often established by determining vendor-specific objective evidence (VSOE).

Notably, determining standalone prices will require a fair amount of judgement from the selling entity, as many organizations do not have robust processes in place for determining prices. To reasonably establish controls, KPMG recommends organizations follow this five-step process.

A discount should be allocated entirely to one or more, but not all, performance obligations in the contract if all of the following criteria are met:

If a discount is allocated entirely to one or more performance obligations in the contract, an entity should allocate the discount before using the residual approach to estimate the standalone selling price of a good or service.

KPMG brings up a few observations, most notably that entities should take a different approach when a large amount of goods and services are bundled in various ways, and to establish a policy for determining what ‘regularly sells’ together.

Variable consideration that is promised in a contract may be attributable to the entire contract or to a specific part of the contract, such as either of the following:

While discussed after the application of discounts in the standard, variable consideration allocation needs to be completed before allocating a discount. For more information, see our discussion on the differences between variable consideration and discounting in our analysis of step 2.

Prices change, and for that, there are certain paths to follow and pitfalls to watch. If and when this does happen, an entity should allocate to the performance obligations in the contract any subsequent changes in the transaction price on the same basis as at contract inception.

Consequently, the transaction price should not be reallocated to reflect changes in standalone selling prices after contract inception. Amounts allocated to a satisfied performance obligation should be recognized as revenue, or as a reduction of revenue, in the period in which the transaction price changes.

A change in the transaction price should be allocated entirely to one or more, but not all, performance obligations or distinct goods or services promised in a series that forms part of a single performance obligation, but only if both of the following criteria are met:

A change in the transaction price that arises as a result of a contract modification should be accounted for in accordance with the guidance on contract modifications. However, for a change in the transaction price that occurs after a contract modification, an entity should apply the guidance in whichever of the following ways is applicable:

16 months may seem like a long time (it’s only five if you’re a public entity), but many organizations are seeing challenges in making the move to implement new processes and systems to meet the requirements of the new standard.

Even if we’re posting monthly blogs leading up to the effective date, you should already be looking at transition methods and other industry-specific considerations that you need to make. To address this, we’ve compiled a list of resources for companies looking to prepare for the upcoming standard:

Sage Intacct recently presented a three-part series on the new standards, which you can view on-demand.

We welcome you to peer through the full text, the AICPA guidance, and to get in contact with us to learn more about preparing for ASC 606 with outsourced accounting services and/or a new accounting software designed with new RevRec Standards in mind.

Financial professionals at growing organizations face a ton of challenges. From ‘doing more with less’ to ‘taking on more roles to support the company and inform executives,’ there is little time to waste. Unfortunately, with this rapid growth comes the fact that there will only be more work to do in the future, and with the talent gap that exists, it’s unlikely you will have the help to do it. This is why it’s important to save time wherever you can and improve the speed and confidence in the way you make decisions.

One of the biggest challenges that growing organizations face is that employees need to do more without adding staff. However, as an organization grows, there are more transactions, more requests from stakeholders, and more numbers to crunch. This means more work inputting data into the accounting software (or worse—spreadsheets), manipulating the data into something useful, and creating actionable outputs in the form of reports.

Speed and automation were just a couple of the eight things you should look for in an accounting software solution. Click the aforementioned link to see part 1, and read part 2 of that blog here.

We briefly recognized lack of speed as one of the top challenges in our blog on knowing when QuickBooks no longer makes the cut, but would like to talk today about why speed and real-time decision-making is so important for organizations looking to jump on new opportunities when the time is right.

The beauty of working at a small business is that you can move faster than an enterprise. Unfortunately this agility can’t be recognized without the right information at the right times.

If you are spending too much time crunching the numbers that your company can’t recognize the first-mover advantage that exists when there are no committees and sub-committees of decision makers and influencers. Real-time decision making requires real-time information, when you need it, where, you need it, and how you need it:

Did you know that nearly every spreadsheet contains errors? If you are driving the decision making at your business with financial metrics, you need to make sure that the numbers are right, as an incorrectly calculated number could mean that you are jumping at an opportunity that you can’t fund, or taking a holding stance when you actually could make a move.

With over 11,000 customers, Intacct has a repeatable, accurate, and efficient way of stacking up the numbers, and has the development capabilities to provide the answers you need.

With APQC estimating that nearly half of a financial professional’s time being spent on transaction processing—making sure the lights are on—they also estimate that only 18% is spent on control, 17% is spent on decision support, and 16% on management activities.

With all this time spent on basic activities, and so little being spent improving the business, there is a lot of room for improvement. Executives want fast, reliable, and concise information about how decision A will impact outcome B.

APQC found that successful companies have worked hard to boost the productivity of their transaction processing, simplifying systems, reducing the number of vendors, employing workflow automation for processes like invoice approvals, streamlining ERP environments, and standardizing to a single chart of accounts.

If you hope to take the steps to reduce the time spent processing transactions so you can get back to improving the business, you need to automate what you can so you can put those skills to better use.

Our latest whitepaper, Taking Your Accounting System to the Next Level, explores some of the warning signs, challenges, and opportunities that organizations face when they outgrow entry-level accounting software. Download the whitepaper here, take your understanding even further by reading the 2017 Buyer’s Guide to Accounting Software on Intacct’s website, or learn more by reading the preview of our whitepaper below.

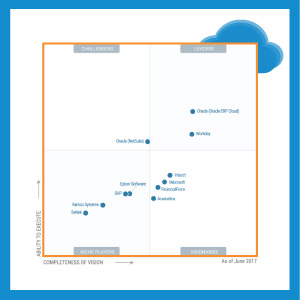

Some shockers, some expected results, and some huge news in the latest Magic Quadrant from the global analyst firm Gartner. In recent weeks, Gartner released a new Magic Quadrant (MQ)—Cloud Core Financial Management Suites for Midsize, Large and Global Enterprises—to help businesses understand the evolving and expanding market that is Cloud ERP.

Up until recently, Gartner avoided building a Magic Quadrant for core cloud finance, due in part to the buying cycle that goes with core financial management applications. Many customers were not looking for an ERP upgrade in recent years, and the immense global players weren’t yet ready to move to the cloud. Now, however, there is a market shift to cloud applications, and CIOs, CFOs, and boards are finding that the cloud offers the security, uptime, and flexibility that they need.

Gartner’s Magic Quadrant reports are a culmination of research in a specific market, giving companies a wide-angle view of the relative positions of the market’s competitors. The reports help prospective buyers quickly ascertain how well technology providers are executing their stated visions and how well they are performing against Gartner’s market view.

Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation.

Gartner saw this, noting that there is a shift from static to dynamic, and there is soon to be $31B in play for cloud financial management and “postmodern ERP.”

“The market for core financial management suites has been static for many years. However, over the last 12 to 18 months, cloud core financial management suites have matured to such an extent that they have disrupted this static market. This reflects the increasing prevalence of postmodern ERP strategies (see “Schrödinger’s Cat: How ERP Is Both Dead and Alive”). Postmodern ERP is the deconstruction of suite-centric, monolithic, on-premises ERP deployments into loosely coupled applications, some of which can be domain suites (such as core financials or HCM) or smaller footprint applications that are integrated as needed.”

For this Magic Quadrant, Gartner defines core financial management suites as follows:

First? The shockers: Some of the largest and well-known players (SAP, Epicor, Deltek) found themselves in the “niche players” category—something that surprised Enterprise Irregulars contributor Vinnie Mirchandani, who said “I honestly cannot remember the last time SAP showed in the lower left quadrant – for niche players – in a Gartner MQ”.

The Expected Results? Global Player Oracle showed up highly on the list for its Oracle ERP Cloud—a solution built to meet the needs of the largest enterprises in the world. This comes as no surprise, as the company displays immense market presence and had begun to make moves to the cloud earlier than many other global software players.

The big news? Intacct was named a visionary, receiving high marks both for its completeness of vision and its ability to execute receiving the third and fourth highest marks, respectively.

Completeness of vision, the more qualitative of the measures, is based on eight components: Market Understanding, Marketing Strategy, Sales Strategy, Product Strategy, Business Model, Vertical/Industry Strategy, Innovation, and Geographic Strategy.

This is a notable victory, but is one that plays into Intacct’s strengths and internal focuses. Intacct has a well-defined mission and business model, and has been known for its success within its market.

While Intacct’s completeness of vision was impressive if not expected, the company’s position on ability to execute is notable, as it exceeded industry giants like SAP, Epicor, Deltek and Microsoft; companies whose operating budgets, global scale, and therefore visibility dwarf Intacct’s.

In fact, when the only companies exceeding the ‘ability to execute’ are two massive publicly traded companies:

Still, with only three vendors who exceed Intacct in ability to execute, Intacct’s notable focus and ability to meet the needs of customers demonstrates the company’s ability to compete and provide a powerful product to growing companies in the middle market, scaling with these customers as they grow.

While many reports will focus on “ERP as a whole,” noting the largest platforms—both cloud and on-premises—this is one of the first reports that looks at applications ranging from midmarket to global, as well as looking at qualitative measures like vision.

One thing Gartner does focus on when talking about Intacct is that while it is able to handle the midmarket, it can also scale with organizations, noting that Intacct’s successes:

This report is normally available only for Gartner clients, but for a limited time, those interested can get the report for free from Intacct’s website.